A late-summer thunderstorm rolls down the Front Range. Hail the size of golf balls hits your Fort Collins roof. Wind tears at a section of siding. By morning, your skylight is cracked and water is dripping into the kitchen. What you do in the next 48 hours decides whether the cleanup costs $3,000 or $30,000. It also decides whether your insurance claim gets paid in full or denied.

Key Takeaways

- The first 48 hours after a Fort Collins storm decide your insurance outcome and total repair cost.

- Document damage before any cleanup, file the claim within 24 hours, and tarp openings to stop further water intrusion.

- Wind and hail account for nearly half of U.S. homeowner insurance claims — Fort Collins sits in Colorado’s Hail Alley.

Why the First 48 Hours Matter So Much in Fort Collins

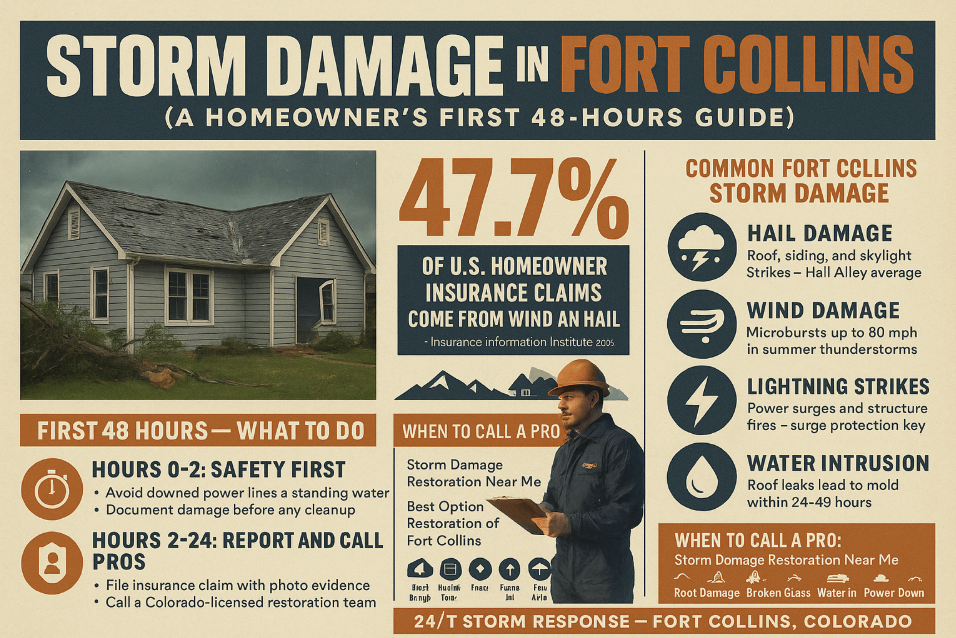

Fort Collins sits in one of the most storm-active corridors in the country. Colorado’s Front Range averages 7-9 severe hail days every year, and according to the Insurance Information Institute, wind and hail account for 47.7 percent of all U.S. homeowner insurance claims by frequency. After a storm hits your home, water intrusion starts immediately. The IICRC water damage standard says drying must begin within 24-48 hours to prevent secondary mold damage.

Insurance carriers also expect prompt action. Most Colorado homeowners policies require notice of loss within a reasonable time — usually 24 to 72 hours. Wait too long, and you risk a coverage denial even on legitimate damage.

Hours 0-2: Safety, Documentation, and Stopping the Bleeding

Step 1: Make sure everyone is safe

Before you check the roof or assess damage, make sure your family is out of harm’s way. Stay clear of any downed power lines. Avoid standing water inside the house — it could be charged from a damaged outlet. Call 911 if you see structural collapse, gas leaks, or active fire.

Step 2: Document everything before you touch a thing

Walk every room with your phone. Take 4-6 photos of each damaged area. Record a slow video sweep of the exterior, including the roof if it’s safe to view from the ground. Capture serial numbers on damaged appliances. Save weather alerts and time-stamped photos to cloud storage. Insurance adjusters lean heavily on this evidence — without it, your claim payout shrinks fast.

Step 3: Tarp openings to stop further water intrusion

If hail or wind broke a window or punctured the roof, cover the opening with plastic sheeting or a tarp. This is called “emergency mitigation” and most insurance policies actually require you to do it. Save receipts for any tarp, plywood, or board-up materials — they’re typically reimbursed under your policy.

Hours 2-24: Insurance and Restoration Calls

Call your insurance carrier first

Get the claim number, the adjuster’s name, and the inspection window in writing. Ask whether your policy covers emergency mitigation services and at what limit. Confirm your hurricane or wind/hail deductible — these are often percentages of your dwelling coverage in Colorado, not flat dollar amounts.

Then call a Colorado-licensed restoration team

After insurance, your next call is the restoration company. Best Option Restoration of Fort Collins provides 24/7 emergency response across Larimer County. Our certified team handles water extraction, structural drying, and direct insurance billing — so you focus on your family while we coordinate with your adjuster.

Searching Storm Damage Restoration Near Me will turn up many options. Verify three things before signing: Colorado contractor licensing, IICRC certification, and whether the company will bill your insurance directly. Best Option Restoration checks all three boxes and is fully familiar with Fort Collins building codes.

Avoid storm-chaser contractors

After major hail events, out-of-state contractors flood the Front Range. Many are unlicensed, demand cash up front, and disappear before warranty issues surface. Always ask for a Colorado contractor license number and verify it on the state DBPR portal before signing anything.

Common Storm Damage Types in Fort Collins

Hail damage to roof and siding

Hail Alley along the Front Range produces large hail several times each summer. Asphalt shingles bruise and crack, leading to leaks within 6-12 months. Vinyl siding cracks. Skylights shatter. Damage often shows up gradually — not always the day of the storm.

Wind and microburst damage

Northern Colorado summer thunderstorms can produce microbursts with wind speeds over 80 mph. These rip shingles, fold gutters, and topple aging trees onto roofs. Wind-driven rain pushes water into wall cavities even when the roof itself looks intact.

Water intrusion and mold risk

Any roof breach starts a 24-48 hour clock to prevent mold. Professional water damage restoration uses thermal imaging and moisture meters to find hidden saturation behind drywall. DIY drying with box fans almost always misses these wall cavities, leading to mold remediation bills weeks or months later.

Lightning strikes and power surges

Lightning damage isn’t always obvious. Power surges fry HVAC control boards, refrigerator compressors, and home electronics. Whole-house surge protectors mitigate this but don’t eliminate the risk. Get an electrician to check your panel after any direct-strike event.

Frequently Asked Questions

How fast must I report storm damage to insurance in Colorado?

Most Colorado homeowners policies require notice within 24 to 72 hours of the loss. Hurricane events shorten this. Call your carrier the same day you can safely access the property and document the call with claim number and rep name.

Can I clean up before the adjuster arrives?

Yes for safety reasons (water removal, debris that blocks exits, tarps over openings). No for cosmetic cleanup. Document everything first with photos and video. Save damaged items for inspection unless they pose a health hazard.

What is the difference between remediation and restoration?

Remediation removes the source of damage — water extraction, mold removal, smoke residue cleanup. Restoration rebuilds the property to its pre-loss condition — drywall replacement, painting, flooring. Most full storm jobs include both phases.

Has Fort Collins ever been hit by a tornado?

Yes. NOAA records show multiple F0/F1 tornadoes in the Fort Collins area since the 1970s. Severe tornadoes are rare here, but hail and microburst wind events are common throughout summer.

Is my neighbor liable for storm damage to my property?

Generally no, in Colorado. Storm damage from natural events is considered an act of nature, and your own homeowners insurance handles it. The exception is when the neighbor’s negligence contributed — for example, an unmaintained dead tree they were warned about that fell during the storm.

Next Steps for Fort Collins Homeowners

The 48-hour window after a Fort Collins storm decides everything that follows. Document fast. Tarp openings. Call your insurance, then a Colorado-licensed restoration team. Skip the storm-chaser contractors. Stop water from sitting in the structure for more than two days.

If a storm just hit your Fort Collins home, call Best Option Restoration of Fort Collins for 24/7 storm damage repair services. Our certified team handles emergency mitigation, full restoration, and insurance documentation in one call.